With GST around the corner, it is extremely critical for businesses to start invoicing under GST mode, and not face any roadblocks, as they usher in the new age. Businesses will need to ensure that the GST transaction invoices are passed with the requisite details, which will later enable them to claim the right ITC and remain GST compliant while growing continuously.

When a registered taxable person supplies taxable goods or services, a GST invoice is issued. To issue and receive a GST compliant invoice is a prerequisite to claim ITC. If a taxpayer does not issue such an invoice to his customer - who is a registered taxable person, his customer loses the ITC claim and the taxpayer loses its customers.

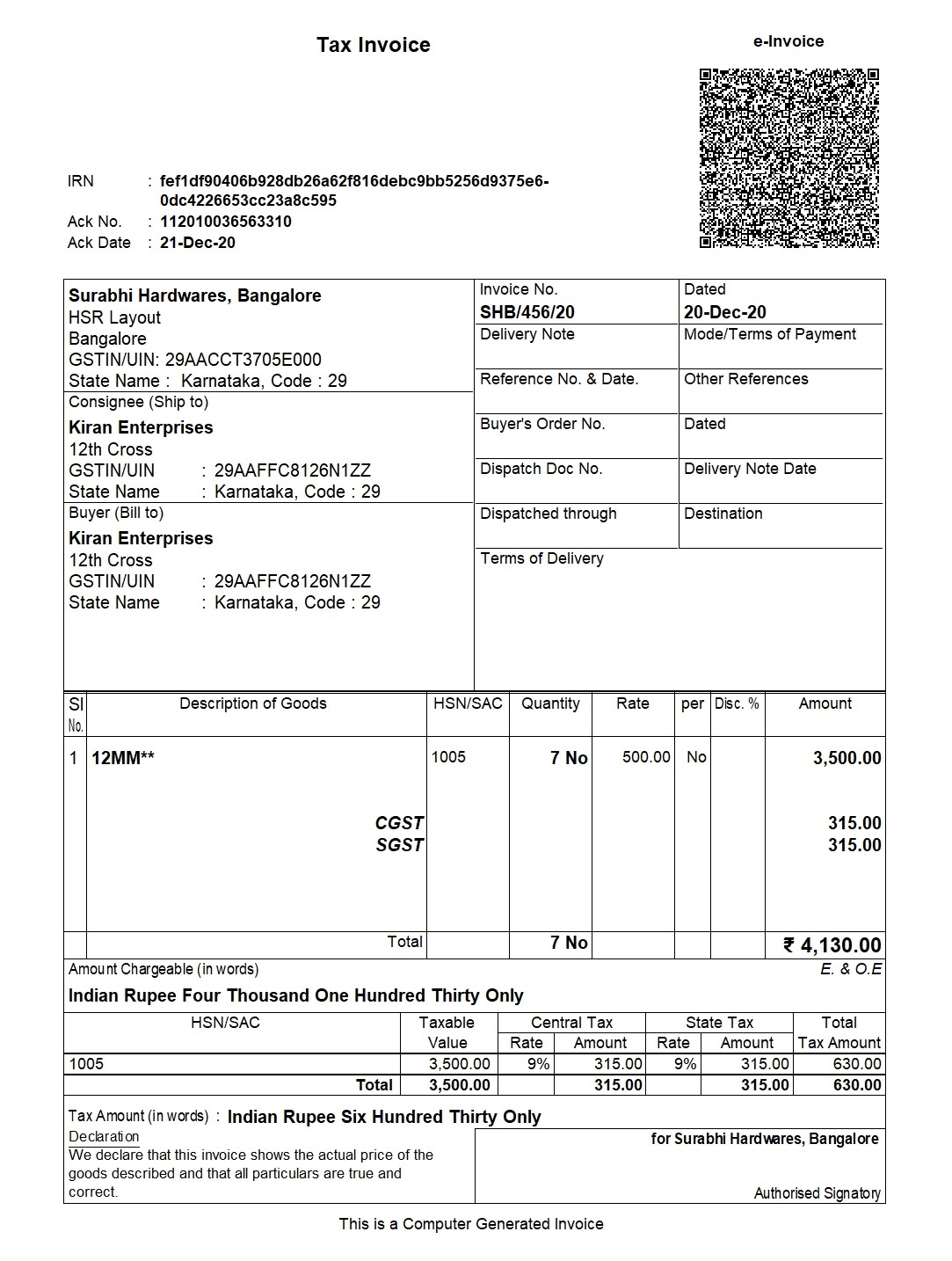

e-Invoice generated in TallyPrime

TallyPrime Release 5.0 with Connected GST Experience

Supply of Goods

Supply of Services

The tax invoice must be issued before or at the time of -

Removal of goods, where the supply involves the movement of goods

Delivery of goods to the recipient, where supply does not require movement of goods

Issue of account statement/ payment, where there is a continuous supply

The tax invoice must be issued within -

30 days from the date of supply of the service

45 days from the date of supply of the service, where the supplier is an insurer or banking company or a financial institution

Supply of Goods

Supply of Services

Original invoice: The original invoice is issued to the receiver, and is marked as 'Original for the recipient'.

Original Invoice: The original copy of the invoice is to be given to the receiver, and is marked as 'Original for the recipient'.

Duplicate copy: The duplicate copy is issued to the transporter, and is marked as 'Duplicate for transporter'. This is not required if the supplier has obtained an invoice reference number. The Invoice reference number is given to a supplier when he uploads a tax invoice issued by him in the GST portal. It is valid for 30 days from the date of upload of the invoice.

Triplicate copy: This copy is retained by the supplier, and is marked as 'Triplicate for supplier'.

Duplicate Copy: The duplicate copy is for the supplier, and is marked as 'Duplicate for supplier'.

A tax invoice need not be issued when the value of the goods or services supplied is less than INR 200 if –

However, a consolidated tax invoice or an aggregate invoice should be prepared at the end of each day for all such supplies for which the tax invoice is not issued.

In case of a registered person purchasing from an 'unregistered supplier', the tax is paid by the recipient, and the recipient must issue an invoice on the date of receipt of goods or services.

When a registered dealer receives an advance payment for a supply, the dealer should issue a receipt voucher for the advance paid by the recipient.

An export invoice must, in addition to the details required in a tax invoice, contain the following details:

Delivery Challan can be issued in some special business cases, such as –

To revise the taxable value or GST charged in an invoice, a debit note or supplementary invoice or credit note must be issued by the supplier.

Debit notes, supplementary invoices and credit notes must include the following details:

Bill of Supply is to be issued by a registered supplier in the following cases:

Similar to tax invoice, a bill of supply need not be issued when the value of goods or services supplied is less than INR 200 unless the receiver insists for the bill. However, a consolidated bill of supply should be prepared at the end of the business day for all such supplies for which the bill of supply is not issued.

The upcoming TallyPrime Release 5.0 introduces a connected GST experience, enabling businesses to handle a wide range of GST activities directly within TallyPrime. From uploading invoices to filing returns and reconciling data, this new release streamlines the entire process. Here's a quick preview of the features you can expect from the new TallyPrime release:

Watch Video on Invoice Matching under GST

Know More about Invoices in GST

E-Way Bill

GST